The Same Mistake, Four Times. About to Be Five.

Every decade or so, the American financial system hands ordinary people the bill for someone else's bad decisions. The faces change. The instruments change. The mechanism does not.

I have lived through four of these cycles. I was inside the fourth one in a way I have not written about publicly before, and I think it is time to.

The Pattern, Walked Forward

The late 1980s. Junk bonds. Michael Milken at Drexel Burnham Lambert pioneered the use of high-yield bonds to finance leveraged buyouts. The bonds paid extraordinary yields because they were rated below investment grade. Pension funds and savings and loans loaded up on them chasing those yields. Drexel collapsed in 1990. Milken was indicted in 1989 and went to prison. The institutions that had bought the bonds, with the public's money behind them, absorbed the losses.

The late 1980s and early 1990s. The savings and loan crisis. Roughly a thousand thrifts failed out of about 3,200, in part because they had been heavy buyers of those same junk bonds, and in part because deregulation had let them make loans they had no business making. The Resolution Trust Corporation was created in 1989 specifically to wind down their assets. Total cost to taxpayers landed around $124 billion. Shareholders were wiped out. Bondholders took losses. The federal deposit insurance fund covered the depositors, which meant the public covered the depositors.

The late 1990s. The dot-com boom. I wrote about this in my piece about taking my Roth IRA to zero on the Palm IPO. Venture capital firms invested in hundreds of internet companies, took most of them public at extraordinary valuations, and cashed out their positions on IPO day. The institutions that ended up holding the stock after the crash were pension funds, mutual funds, insurance companies, and 401(k)s. The smart money got out. The public held the losses.

The mid 2000s. The financial crisis. This is the one I sat inside of.

What I Did and Why It Matters

I spent the years leading up to the financial crisis in capital markets, working on securitizations. That is the business of taking a pool of loans, packaging them into bonds, and selling those bonds to institutional investors. I had a direct relationship with the firms creating these structures, and I had a direct view into how the system worked. I am not writing this as someone who watched the crisis on television. I am writing this as someone who participated in the machine that produced it.

The popular memory of 2008 blames the lenders for making bad loans. Subprime mortgages. Stated income loans, also known inside the industry as liar loans, where the borrower told the lender what they earned and the lender accepted it. At one point there were 125 percent loan-to-value home equity loans on the market, which gave a borrower more money than the home was worth. Those products were genuinely reckless.

But blaming the lenders is only a partial story, and it lets the much bigger players off the hook.

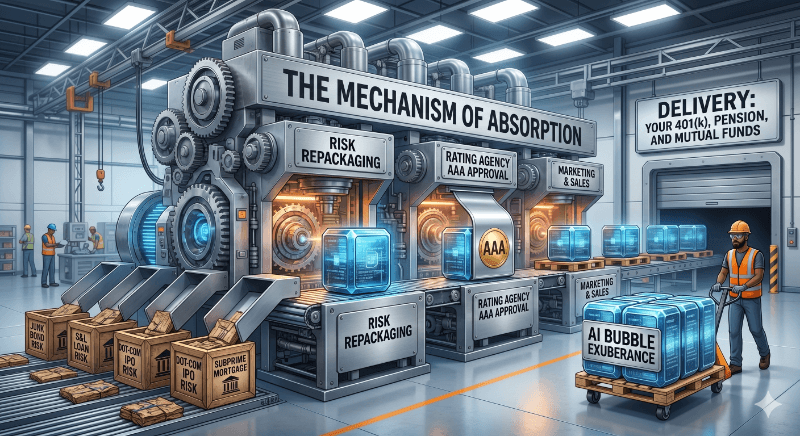

Here is how the actual machine worked. Mortgage companies and banks originated loans, but they did it by borrowing short-term money to fund those loans. To pay back the short-term money, they sold the loans into the capital markets. Investment banks bought the loans, packaged them into bonds called mortgage-backed securities, and sold the bonds to pension funds, insurance companies, mutual funds, and 401(k)s. The rating agencies, who were paid by the issuers of the bonds, rated the senior portions of these structures AAA, the same rating as US Treasuries.

The originator did not care if the borrower could pay, because the originator was selling the loan within ninety days. The investment bank did not care if the borrower could pay, because the investment bank was selling the bond within ninety days. The rating agency did not care if the borrower could pay, because the rating agency was being paid to rate the bond, not to be right about it.

The only people in the chain who would end up caring deeply about whether the borrower could pay were the institutions that bought the bonds. Pension funds. Insurance companies. Mutual funds. 401(k)s. The same places that ended up holding pets.com stock in 2001. The same places that ended up holding savings and loan bonds in 1991. The same places where ordinary people's money quietly accumulates.

When the borrowers stopped paying, the bonds stopped paying. The ratings turned out to be wrong. The institutions took the losses. Some of those institutions needed federal bailouts to survive, which meant taxpayers took the losses. The originators had collected their fees and were gone. The investment banks had collected their fees and were either bailed out or absorbed. The rating agencies paid relatively small fines and kept their business model intact.

The bill landed exactly where it always lands.

What Is Happening Right Now

There is a company called Luel that just raised $31.2 million in seed funding led by General Catalyst and Lightspeed Venture Partners, one of the largest seed rounds in Y Combinator's history. Luel was founded in 2025. According to its own announcement, it has been operating for months. According to public reporting in AOL's coverage of the situation, the founder of an existing competitor in the same space, a company called Kled, has publicly alleged that Luel's website appeared almost identical to his, that he had taken multiple meetings with General Catalyst before Luel was funded, and that the new round went to what he described as a copycat. Kled itself had raised $5.5 million in its own seed round before Luel emerged.

I am not making any claim about the merits of either company. I have no inside information about either one. The dispute is being adjudicated publicly and that is where it belongs.

What I can say is that a $31.2 million seed round, into a months-old company, in a space where an existing competitor with a similar product is alleging the new entrant copied it, is exactly the kind of decision-making that defined the late stages of every prior cycle I have lived through. The diligence is compressed. The exuberance is replacing the analysis. The capital is moving faster than the verification.

I do not know how Luel turns out. I do not know how Kled turns out. What I do know is that when the dust settles on this AI cycle, the bag will land where the bag always lands. It will land in the pension funds and mutual funds and insurance company portfolios that hold the eventual public stock of whichever of these companies make it to an IPO, and the ones that bought late at the wrong price.

What Has Not Changed

The mechanism that produced the junk bond collapse, the savings and loan crisis, the dot-com bust, and the financial crisis is the same mechanism that will produce the AI correction. Risk gets manufactured by people who are paid to manufacture it. It gets repackaged by people who are paid to repackage it. It gets rated, marketed, sold, and finally absorbed by institutions that are managing other people's money. When the bets go bad, the people whose money was being managed pay for it.

I worked inside that machine for over a decade. I left because I could see where it was going. The crisis arrived two years later, exactly the way the math said it would.

I am writing this now because I see the same shape forming, on a much larger scale, in AI. The technology is real. I have said before and I will keep saying that it is the most important technology shift of our lifetimes. But the technology being real does not protect the public from the way the financial system processes the technology. Every previous cycle has proven that point at the public's expense. There is nothing in the current cycle that suggests this one will be different.

The bill is being prepared. It will arrive in the usual place.

If you have a view on this, drop a comment below or send me a DM.