How I Took My Roth IRA to Zero. And What I Am Watching Now.

In March 2000, I put my entire Roth IRA into one stock.

I am a recovering investment banker now. Back then I was just an investment banker. I had spent the dot-com boom getting allocations at the IPO price, watching the stock double on the first day, selling, and repeating. Amazon. eBay. Autobytel. Dozens of others. Some of those positions would be worth millions today if I had held them. Many went to zero, so taking the short-term gains was the right call on most of the trades. The strategy was simple: buy at the IPO price, sell into the pop, do it again next month.

The reason I got those allocations is that my company had a significant business relationship with Credit Suisse First Boston, which was run on the technology side by Frank Quattrone, the most powerful tech banker of the era. Quattrone's group took Amazon, Netscape, and Cisco public. He was reportedly making nine figures a year. After the bubble burst he was indicted on charges related to how IPO shares had been allocated to favored clients. He was eventually vindicated, but his career and the industry around him were never the same. I was a small participant in the system Quattrone sat at the top of, and that participation was what gave me access to the deals I was flipping.

The Roth IRA was a brand new financial product at that point. Congress had created it as part of the Taxpayer Relief Act of 1997, and the first year anyone could actually fund one was 1998. So when I made this trade in March 2000, I had been contributing to a Roth IRA for two years total. The contribution limit was $2,000 per year. The whole account had maybe $4,000 in it.

And I decided I was going to use all of it to buy Palm Inc. on its first day of trading.

I loved the Palm Pilot. I used mine every day. It had the calendar, the contacts, the notes, the to-do lists. It was basically the iPhone, a decade too early. The product was great. The thesis felt obvious to me.

I did not get an IPO allocation on Palm. So I put in a buy order for the open instead. Whatever the open was, that was my price.

Palm priced its IPO at $38 a share. It opened the next morning at $145. By the close of the first day, it was at $95. My buy order filled at the open. I watched the position lose more than a third of its value in a single afternoon, on the same day I bought it.

I held. There was no other choice. Within a year, Palm was under $20. The IRA went to zero.

I am telling this story because I see a version of the same setup forming right now, and I think a lot of people who have never been on the wrong side of one of these are about to learn what it feels like.

What Actually Happened in 2000

The dot-com era from the inside looked different than it looks in the history books.

VCs invested in hundreds of companies that ended up with an exit. Almost all of them went public. That changes everything. Instead of private equity and venture capital firms losing money when their bets did not work out, they cashed out at the IPO. The companies went public, the wealthy investors took their money off the table, and the public markets absorbed the position.

Individual investors. Pension funds. Mutual funds. The 401(k)s of regular people. That is who ended up holding the bag when the music stopped.

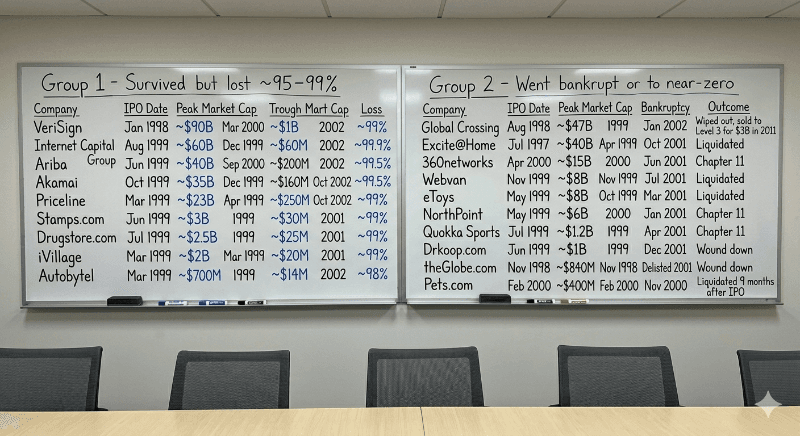

Pets.com is the textbook example. They went public in February 2000 at $11 a share. They had no path to profitability. The cost to ship a 40-pound bag of dog food made the unit economics impossible. By November 2000, the company was liquidating and the stock was worthless. Yes, Chewy is a real business today. But Chewy exists in a post-Amazon shipping world that did not exist when Pets.com tried it.

Pets.com gets the punch line, but it was not the only one. There was a company called Kozmo that was trying to do same-day delivery of everything from snacks to videos. Twenty years before DoorDash. The idea was right. The technology and the cost structure were wrong. There was Autobytel, the Carvana of its era, which I had also gotten on the IPO. Great idea, wrong decade.

The story of 2000 is the story of how wealth transferred from private market participants who knew exactly what they were holding to public market participants who did not.

How You Could Tell, If You Were Looking

People say bubbles are only obvious in hindsight. That has not been my experience.

I watched the mortgage market in 2006 and 2007, with the rating agencies handing out AAA ratings on bonds whose underlying collateral was clearly mispriced. I lived the dot-com cycle in real time. The pattern is similar every time, and the warning signs are not subtle.

Valuations get to levels where the future revenue required to justify them is no longer plausible. The math stops working. Sophisticated investors know it. They keep buying anyway because the next person will pay more, and the exit through an IPO is still open. Memories are short. FOMO takes over. Capital floods in. Most of the bets in venture-style investing at this stage are home runs or strikeouts. There are very few singles or doubles. The home runs make up for the strikeouts, and that math holds right up until the moment it does not.

The 2000 era had this dynamic everywhere. Companies were going public at valuations that would have required twenty years of perfect execution to make sense. Everyone knew. Nobody cared, because everyone was getting out at the IPO.

What I Want To Say Before I Get Into AI

I am about to write a second piece on the AI market specifically, and I want to be clear about something before I do.

AI is not a fad. AI is going to create more value than any technology in history. I wrote about why I believe that in February in Moore's Law on Steroids, and I am not going to rehash that argument here. The short version is that the technology that powered the last fifty years of computing has run out of room, and AI has started a new and faster cycle in its place. The transformation is real. I am betting my career on it.

The dot-com era, with the exception of Amazon and its eventual creation of AWS, was largely about putting commerce online. Buying pet food. Buying books. Buying cars. AI is not that. AI is going to remake every part of how humans work, learn, build, and connect. The technology is more important. The economic value created over the long run will dwarf what came out of the late 1990s.

But the technology being real does not mean the prices are right. Those are two different questions. The first one is settled. The second one is where this gets interesting.

In my next piece, I will tell you where I think the real risk is in the AI market today. It is not where the headlines say it is. The trillion-dollar names everyone is watching are not actually the most dangerous bet. The danger is a layer below them, and it is much bigger than most people realize.

If you lived through a previous bubble cycle, I am curious what the moment was when you first realized something was off. Reach out at hello@kenektic.com.